2026–27 Federal Budget: Major Tax Changes Ahead

The Australian Government recently announced the 2026–27 Federal Budget on 12 May 2026. The Budget introduces several major proposed tax reforms that may significantly affect property investors, businesses, family trusts, and individual taxpayers.

Foreign Investors

The Government has extended the temporary ban preventing foreign investors (non-Australian citizens and non-permanent residents) from purchasing established residential properties until 30 June 2029.

Capital Gains Tax (CGT) Reform

1. Removal of the 50% CGT Discount

From 1 July 2027, the current 50% CGT discount for assets held longer than 12 months will be replaced with a CPI indexation method.

Under the proposed rules:

Capital gains accrued up to 30 June 2027 will continue to receive the existing CGT discount treatment.

Any increase in value after 1 July 2027 will use the new indexation method instead.

In addition, pre-CGT assets (assets acquired before 20 September 1985), which are currently exempt from CGT, will become subject to CGT on gains accruing from 1 July 2027 onwards.

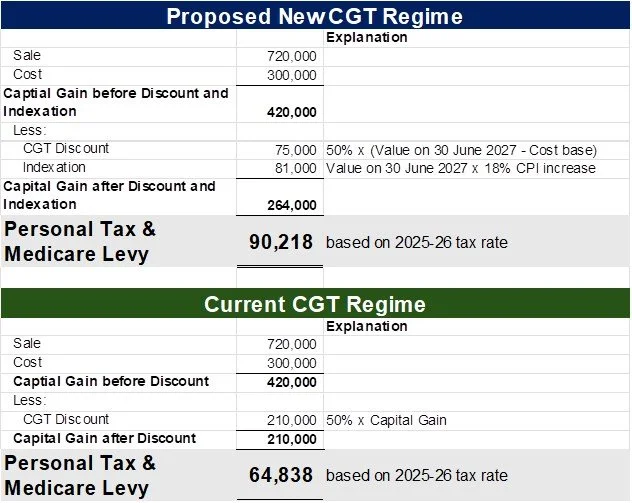

Example

John acquired an investment property on 7 April 2022 for $300,000 and later sold it on 29 September 2031 for $720,000.

Assumptions:

• Property value on 30 June 2027: $450,000

• CPI indexation between 1 July 2027 and 29 September 2031: 18%

• John has no other taxable income in the 2032 financial year

Based on the proposed rules, John is expected to pay approximately $25,380 more in tax and Medicare levy compared with the current system.

2. Minimum 30% Tax on Capital Gains

From 1 July 2027, the Government proposes introducing a minimum 30% tax rate on indexed capital gains.

This means taxpayers whose effective tax rate on capital gains would otherwise be below 30% may pay additional tax.

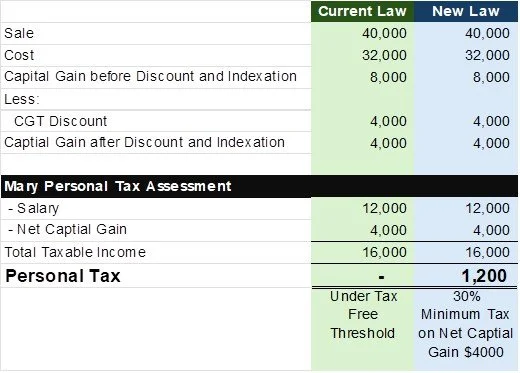

Example

Mary purchased US shares for AUD 32,000 on 22 August 2025 and sold them for AUD 40,000 on 1 July 2027.

Assumptions:

Mary earns part-time employment income of $12,000 during the year

Share value remained unchanged between 30 June 2027 and 1 July 2027

Although Mary is a low-income earner, she may still need to pay approximately $1,200 tax on the capital gain under the proposed minimum tax rules.

The End of Negative Gearing for Established Residential Property

From 1 July 2027, rental losses from established residential properties acquired after 12 May 2026 will no longer be deductible against salary or other personal income.

Negative Gearing tax saving strategy might soon be restricted.

Instead:

losses will be carried forward; and

can only be offset against future rental profits or capital gains from residential property.

However, the following will generally remain unaffected:

newly built residential properties;

commercial properties;

properties acquired before 12 May 2026;

certain build-to-rent developments;

some widely held trusts and superannuation funds.

The Government has also provided a transitional period. Properties acquired between 12 May 2026 and 30 June 2027 may still access negative gearing deductions until 30 June 2027.

Minimum 30% Tax on Discretionary (Family) Trusts

From 1 July 2028, discretionary trusts (commonly known as family trusts) will be subject to a minimum tax rate of 30% on trust income.

Beneficiaries other than corporate beneficiaries may receive non-refundable tax credits for tax already paid by the trustee. Therefore traditional bucket company arrangement might not be working.

This means low-income beneficiaries may no longer be able to receive refunds of excess tax paid by the trust, unlike company franking credits which may be refundable depending on the shareholder’s tax position.

To assist restructuring, the Government will provide temporary rollover relief between 1 July 2027 and 30 June 2030 to allow eligible trusts to transition into alternative entity structures such as companies.

Business Measures

Permanent $20,000 Instant Asset Write-Off

From 1 July 2026, the $20,000 instant asset write-off for small businesses with turnover under $10 million will become permanent.

Monthly PAYG Instalments

From 1 July 2027, eligible small and medium businesses may choose to report and pay PAYG instalments monthly.

Loss Carry-Back for Companies

From 1 July 2026, companies with annual global turnover below $1 billion will be able to carry back eligible revenue tax losses for up to two years.

Eligible start-up companies may also access refundable tax offsets based on qualifying tax losses.

Electric Vehicle (EV) Fringe Benefits Tax (FBT) Changes

Eligible electric vehicles currently receive a full FBT exemption where the vehicle value falls below the fuel-efficient luxury car tax threshold.

FBT concession on Electric Vehicle will be reduced.

From 1 April 2029:

a permanent 25% FBT concession will apply instead of the current full exemption; and

this will be implemented through a reduced statutory formula rate.

Transitional rules will apply:

existing arrangements may retain their current concession; and

EVs provided before 1 April 2029 with a value below $75,000 may continue receiving full exemption treatment.

Personal Tax Measures

1. Working Australians Tax Offset (WATO) $250

From 1 July 2027, individuals earning employment income or sole trader business income may receive a new $250 tax offset.

2. Instant Work-Related Deduction $1,000

From 1 July 2026, Australian tax residents earning employment income may claim up to $1,000 of work-related deductions without keeping receipts.

This standard deduction will cover ordinary work-related expenses such as:

home office expenses;

laundry;

work-related travel; and

similar employment expenses.

Other deductions such as:

charitable donations; and

union or professional membership fees

can still be claimed separately on top of the $1,000 deduction.

Taxpayers with work-related expenses exceeding $1,000 may still claim actual deductions under the normal substantiation rules, provided appropriate records are maintained.

Final Thoughts

These proposed reforms represent some of the most significant tax changes announced in recent decades and may substantially affect investment decisions, business structures, and tax planning strategies.

As many of these measures are not yet legislated, further consultation and changes may still occur before the final laws are passed.

If you would like advice on how these proposed changes may affect your personal or business circumstances, please feel free to contact us.